Image source: Getty Images

With low interest rates and geopolitical tensions sending shivers through markets, the outlook for UK stocks is changing.

with Lloyd’s‘(LSE:LLOY) Shares are often seen as an indicator of the local market, so I decided to see where analysts thought they might go next year.

Looking forward

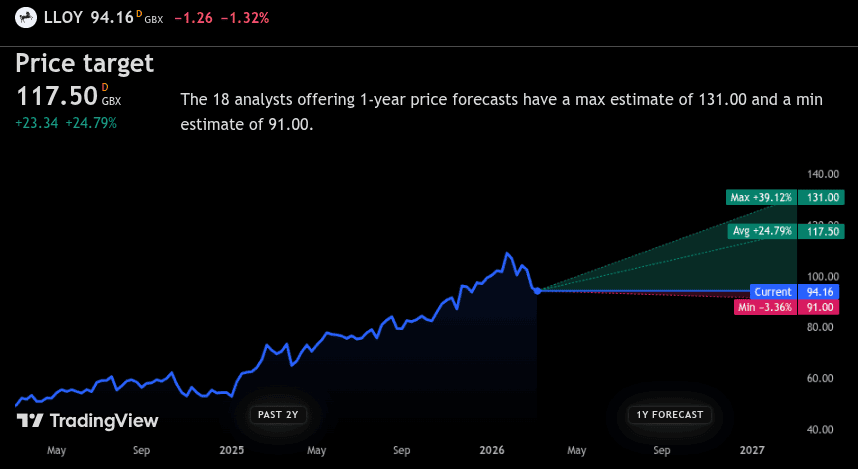

Analysts following Lloyds have an average 12-month price target of 117.5p, which represents an increase of 24.92% from today’s level. If that happened, the £1,000 would grow to approximately £1,250 from the shares alone. Add in a dividend yield of 6% and the total return could approach 30%, or around £1,300 (before dealing with costs and taxes).

On the optimistic side, some analysts believe that the price could rise by about 39.27%. In this case, the £1,000 could rise to approximately £1,390 from the share price alone, or approximately £1,450 including dividends.

On the pessimistic end, the gloomiest forecast is for a price decline of 3.29%. Even then, dividends can still leave an investor roughly flat or slightly ahead over the course of the year.

To get a better idea of where this might be headed, I took a closer look.

Fundamentals and key earnings

Over the past five years, the Lloyds share price has risen by almost 125% – a very strong rise for mature bank stocks. But revenue is the real story here, a clear signal of the benefits of a higher interest rate environment. It has doubled since 2022, rising from £26.2 billion to £65.55 billion.

What does this mean for shareholders? Well, the return on equity (ROE) isn’t amazing – it’s just over 10%, which is broadly in line with many major lenders. But what Lloyds usually wins is income.

The stock currently offers a dividend yield of just under 6%, and the payout uses only about 52% of earnings – so it’s well covered. Plus, it’s backed by 12 years of continuous payments, adding a degree of reassurance for those targeting passive income.

Overall background and risks

As a largely domestic bank, Lloyds has significant exposure to the health of UK consumers and businesses. The main driver of growth in recent years has been interest rates. But after several cuts, the Bank of England’s base interest rate is now around 3.75%, with further cuts expected.

This presents a mixed picture for Lloyds. Low interest rates can put pressure on lending margins, but they also support the housing market and keep bad debts under control. But if the economy slows or unemployment rises faster than expected, profits could come under pressure.

However, it has been able to tie dividends to significant share buybacks.

Final thoughts

For a British investor looking to open a new investment account in April, Lloyds still looks attractive. It’s a big, familiar bank with a great dividend yield and analyst forecasts of modest share price growth over the next year. The bank is profitable, well capitalized, and returns a lot of cash to shareholders.

However, this is still a cyclical share closely linked to the fortunes of the UK economy. Anyone buying today should be prepared for bumps along the way – especially if growth disappoints or the housing market turns.

For investors who are comfortable with this risk, it provides income as well as some potential positive price movement. But it’s just one of several high-yielding FTSE stocks to consider in the UK market today.