Image source: Getty Images

A monthly passive income of £1,000 – £12,000 a year – sounds like something reserved for people who already have a lot of money. But this is not the case.

With a stocks and shares ISA and a long enough runway, it is a realistic goal for ordinary investors. The mechanism that makes this possible is the compound, and it’s worth understanding it properly before we get to the numbers.

Start early, believe double

Compounding is simply what happens when returns depend on past returns. Reinvest your dividends (or invest in growth stocks that essentially do this for you – they reinvest company profits) and next year you’ll earn income from a slightly larger property. Watch the stock price rise and future gains come from a higher base. Nothing complicated, but give it 10 years and the effect will become very noticeable indeed.

However, worsening begins to appear after a relatively short period of time.

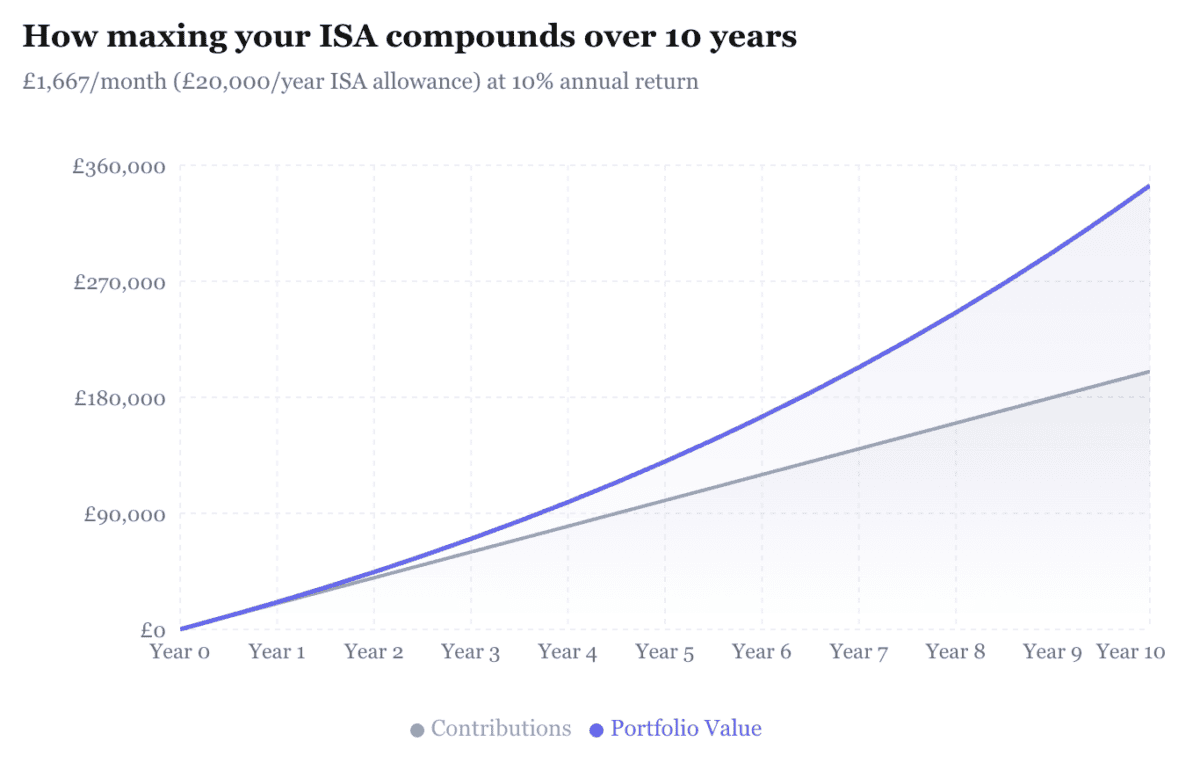

The annual ISA allowance is £20,000, so someone who maxes out each year would put away £200,000 over a decade before investment returns are taken into account. At an annual return of 10% – roughly what global stock markets have averaged historically, although with plenty of bumpy years along the way – regular monthly contributions of around £1,667 would double to around £300,000 over 10 years.

So, how much do you actually need to make to make £12,000 a year? The answer depends on the return. Personally, I believe a 5% dividend yield is very achievable and sustainable with the right stocks. This would indicate that the investor needs £240,000 in the portfolio.

There are no guaranteed profits and markets do not move in straight lines…but that is the theory.

Put that money to work

Beyond theory, novice investors need to think about where to invest this money. The combination of diversification and conviction is a popular strategy. Growth-oriented stocks are arguably the best way to increase portfolio size – but the risks can be greater here.

One stock I find really compelling right now is… Sanmina Company (NASDAQ:SANEM). The US-listed electronics manufacturer sits at the intersection of cloud computing, AI infrastructure and advanced industrial systems – yet the market doesn’t seem to have fully priced it in.

Shares trade at about 11.7 times forward earnings, about 45% below the sector average. With medium-term earnings growth estimated at around 26% per year, the implied P/E/G ratio of around 0.49 suggests that the growth story is not fully reflected in the price.

For context, Celestica — a very similar business I invested in more than three years ago — now trades at 29 times forward earnings after rising more than 3,000% in five years. Sanmina looks like Celestica did before the market exploded.

The main risk is the balance sheet. The upcoming acquisition of ZT Systems’ data center manufacturing business from AMD will push net debt toward $2 billion, leaving the company more vulnerable if AI spending slows.

However, I fully believe this company is worthy of attention.